07. Attribution Reporting

Attribution Reporting

Let's take this opportunity to look at an example attribution report in a fund's documentation.

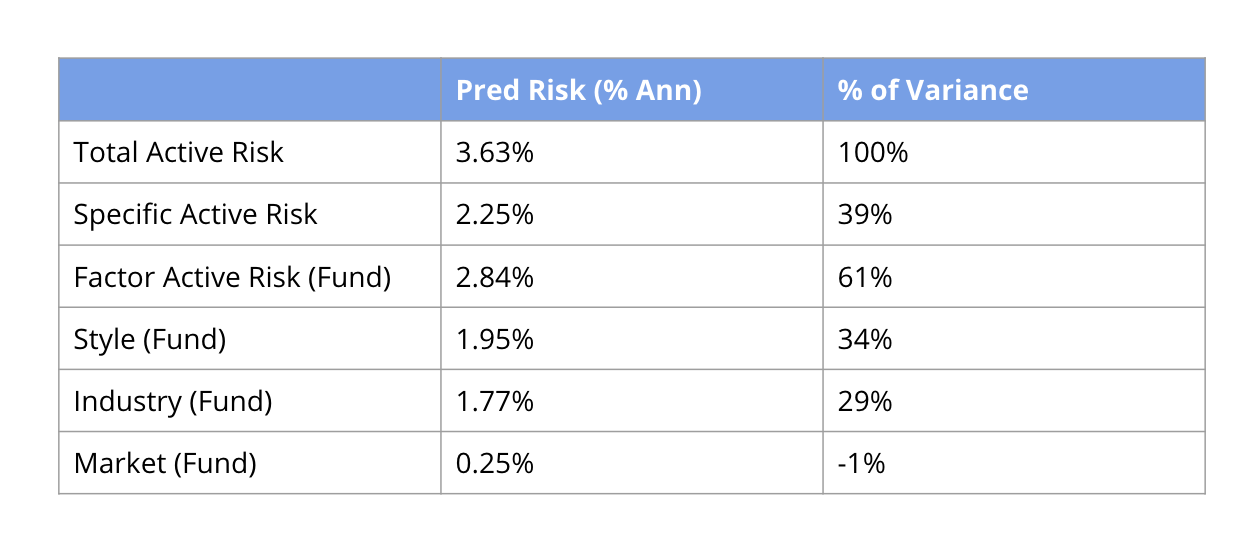

In this first example, we can see the risk of a portfolio decomposed using a fundamental risk model. Fundamental factors are factors based on common sources of risk. Their meaning remains the same over time, even if the factor exposures are updated daily. The total predicted active risk of 3.63% annual volatility can be split into a specific/idiosyncratic component, which accounts for 39% of variance (as calculated using a variance decomposition), and a factor component, which can be further split into the contributions of 3 fundamental factors.

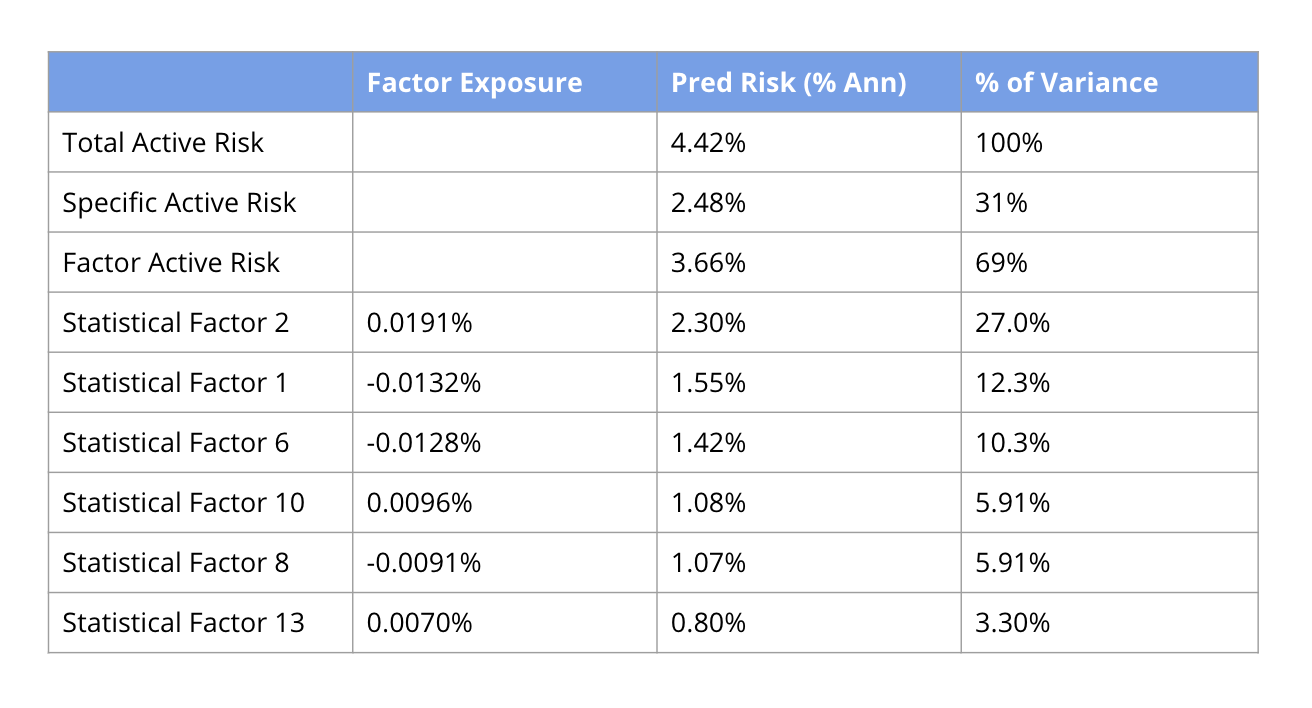

You can do the same sort of attribution with statistical risk factors, but the individual risk factors are hard to interpret. In the example below, most of the risk is attributed to Statistical Factors 2, 1 and 6, however this does not immediately provide a lot of insight. Additional analysis would seek to understand whether other, interpretable factors are similar to Statistical Factor 6.